Trudeau gov’t refuses disclosure of production cap costs

Mostbet Giriş Güncel Adresi 2024 ️ Most Bet On Line Casino Ve Bahi

noviembre 15, 20221xBet Azərbaycan: rəsmi saytın nəzərdən keçirilməs

noviembre 17, 2022Trudeau gov’t refuses disclosure of production cap costs

This report is used to determine the cost of goods sold and to determine the value of inventory. The cost of production report is commonly used in process costing systems where goods are produced through a series of processes and not produced individually. The 750 shells in production at the end of January were 60% complete as to conversion costs and 100% complete as to direct materials, so in February they will need 40% more conversion but 0% more direct materials. It’s a measurement to ensure that activities are performed correctly the first time to avoid the need for rework, which takes time and adds costs to production.

Step 2 of 3

That is, the maximum level of production output that can be produced without lowering the quality of the finished goods, increasing their production cost or extending the production schedule. Scheduling production, planning a budget and allocating resources only sets up manufacturing for success. Monitoring and controlling that process ensures that deadlines are met and costs aren’t exceeded. One way to keep track of the manufacturing process is with a production report. The cost of production report first accounts for the number of units in the department’s beginning WIP and transferred into the department during the period. A manufacturing company that used cost reporting to identify and eliminate sources of variance and improve product quality.

To Ensure One Vote Per Person, Please Include the Following Info

- The revision should make any necessary corrections, adjustments, or improvements to the cost report.

- Generate status, workload, timesheet, variance and other reports in just a keystroke.

- But he will be entering the White House after what will almost certainly be the hottest year on record in 2024.

- The Department of Environment did not disclose the regulatory text that includes a Regulatory Impact Analysis Statement outlining costs, reported Blacklock’s Reporter.

- This inventory category is essential for understanding the efficiency and effectiveness of a manufacturing operation.

Therefore, there will generally be some work-in-process inventories at the end of each month. Production reports seek efficiencies and one area that can always be improved is resources. At this point, their availability can be set, such as vacation days, PTO and global holidays. Use the team page or color-coded workload chart to see the team’s allocation and balance their workload to keep them working at capacity. Mark P. Holtzman, PhD, CPA, is Chair of the Department of Accounting and Taxation at Seton Hall University. He has taught accounting at the college level for 17 years and runs the Accountinator website at , which gives practical accounting advice to entrepreneurs.

Do you already work with a financial advisor?

By identifying the root cause, the company can take corrective actions such as negotiating better material prices, investing in employee training, or optimizing energy consumption. From a managerial perspective, the allocation of manufacturing overhead is about more than just numbers; it’s about understanding turbotax live 2021 cost behavior and making informed decisions. Managers need to understand how overhead costs behave in relation to changes in production levels to manage costs effectively. The cost of production is a complex and dynamic element that requires careful consideration and strategic management.

Cost of Production Report (CPR) Questions and Answers FAQs

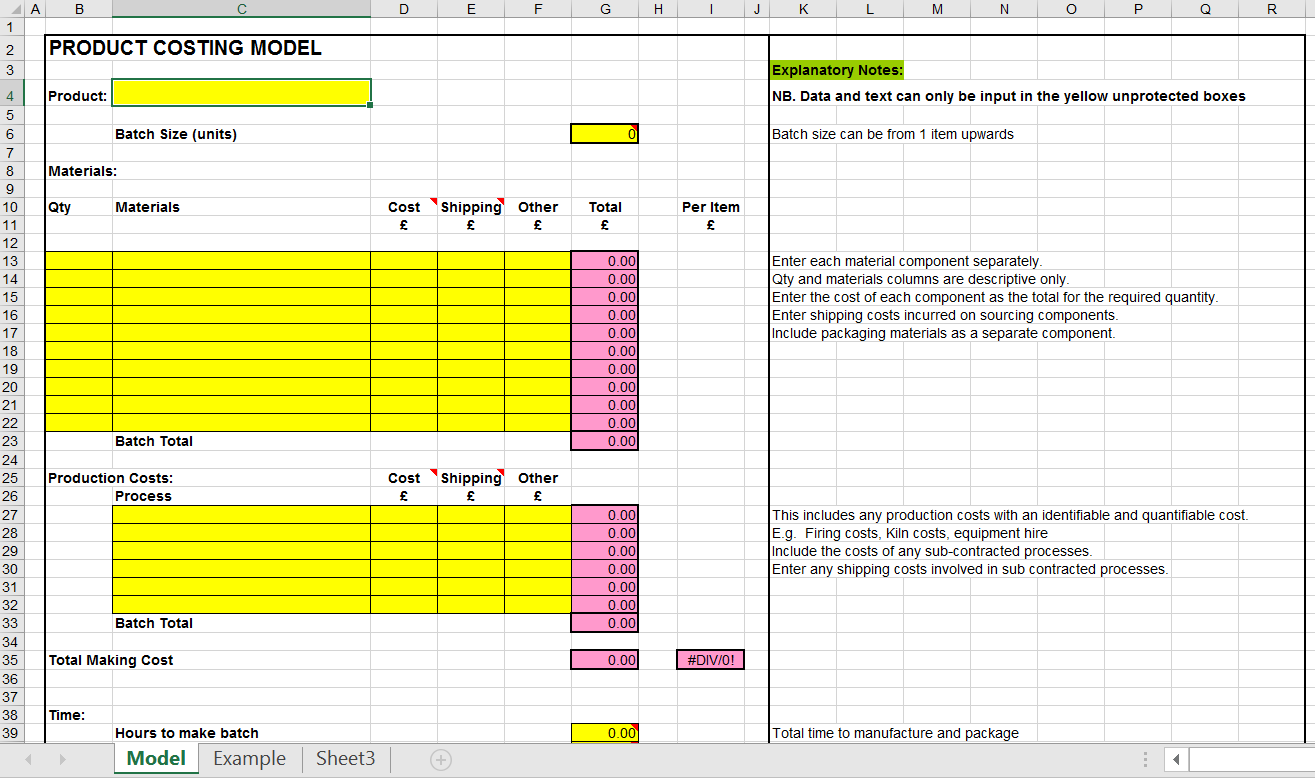

The production costreport summarizes the production and cost activity within aprocessing department for a reporting period. Rounding the cost perequivalent unit to the nearest thousandth will minimize roundingdifferences when reconciling costs to be accounted for in step 2with costs accounted for in step 4. 24,000 units were received from the first department during May. 14,000 units were completed and transferred to the finished goods store room, and 10,000 units were still in process at the end of May. The units in work-in-process ending inventory were 50% complete with respect to materials and 25% complete with respect to labor and manufacturing overhead costs. The data can be collected from various sources, such as the accounting system, the project management software, the invoices, the receipts, the timesheets, and the contracts.

6: Preparing a Production Cost Report

This means checking the accuracy, completeness, and reliability of the cost report, as well as the compliance with the rules and regulations. The cost report should be reviewed and validated by the project manager, the client, the accountant, and the auditor, depending on the scope and objective of the report. The review and validation process may involve feedback, corrections, adjustments, and approvals. For example, a cost report for a grant-funded project may require more review and validation than a cost report for an internal project.

This is because the $62 unit cost includesboth variable and fixed costs (see Chapter 5 for a detaileddiscussion of fixed and variable costs). The cost report is a crucial document that summarizes the financial performance of a project or a business. It helps to monitor the budget, track the expenses, identify the variances, and evaluate the profitability. A well-prepared and well-presented cost report can provide valuable insights to the stakeholders, such as the project manager, the client, the sponsor, the accountant, and the auditor. In this section, we will discuss some of the best practices for preparing and presenting a cost report, as well as some of the common challenges and pitfalls to avoid. We will also suggest some of the next steps that can be taken after completing a cost report, such as reviewing the lessons learned, implementing the corrective actions, and celebrating the achievements.

A financial analyst might use COGM as a key indicator of a company’s efficiency. By comparing COGM with total sales, analysts can assess the gross margin and determine if a company is managing its production costs effectively. A manufacturing KPI is a metric to understand the efficiency of the production process. It should reflect strategic goals, be quantifiable and measurable, but also attainable and actionable. The following is a project report example of those fundamental manufacturing KPIs that production managers track.

A clear scope and objective will help to determine the level of detail, frequency, and presentation of the report. For a marketing strategist, understanding the cost of production is key to formulating a value proposition. If a product is more expensive to produce but offers unique benefits, marketing can craft messages that justify the premium price. A production manager, on the other hand, might use this data to assess the performance of different production lines or shifts. They could implement process improvements or lean manufacturing techniques to reduce waste and increase efficiency. From an accountant’s perspective, COGS is a key figure for calculating gross profit, which is done by subtracting COGS from revenue.

The cost reporting system enabled the company to identify the sources and causes of variance, such as material waste, machine downtime, labor inefficiency, and quality issues. The company then used this information to implement corrective actions, such as improving inventory management, optimizing machine settings, training and motivating workers, and enforcing quality standards. As a result, the company was able to reduce variance costs by 25%, improve product quality by 15%, and increase customer satisfaction by 20%. The cost reporting system also helped the company to evaluate the profitability and competitiveness of each part, and to make informed decisions about pricing, product mix, and market segments. From a financial perspective, analyzing cost data helps in assessing the overall financial health of a business. By examining cost trends over time, financial analysts can identify cost drivers, such as changes in raw material prices or labor costs, and evaluate their impact on the company’s financial performance.

By integrating cost of production data into strategic decision-making, companies can create a robust framework for operational excellence and long-term profitability. This data-driven approach enables a proactive stance, allowing businesses to anticipate changes and adapt swiftly in a dynamic market landscape. It’s the compass that guides a company through the complex waters of production economics, ensuring that every decision is backed by solid data and a clear understanding of the cost implications.